Creating a Trillion-Dollar House of Cards

The AI bubble and how short circular investments are creating an unprecedented investment boom, with over $1.4 trillion in committed spending across a tightly interconnected network of companies.

At the center of this ecosystem lies an, let’s call it “interesting”, pattern: the same money appears to be circulating between a handful of players, creating what critics warn could be the largest financial bubble since the dot-com crash of 2000.

Necessary Intro

I think it is important to explain shortly how markets and businesses work. Usually, if you buy something, money is distributed and allows others to spend money. However, if we zoom very far out, money always runs in circles. But just on such a big scale, we will practically never see the same coin again.

So let’s say you go with a friend to drink a coffee. 20 bucks gone. The cafe owner pays from this the coffee beans, water, electricity, someone for marketing, a credit, the employees, a nearby grocery store etc. And from here your 20 bucks keep distributing. E.g. the employee is saving money to buy a bicycle. A new breakdown starts. And so on. The entire market is connected, and the scale is difficult to imagine, but it is huge. Therefore, money that flows is good for everyone.

Now, what we are going to talk about today are very short cycles. So short that you will see the same coin multiple times.

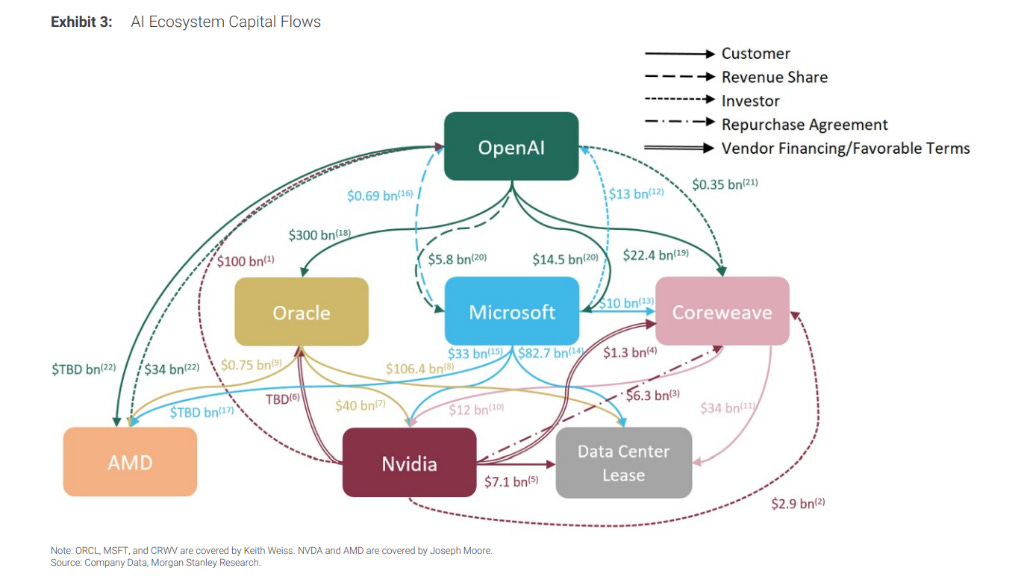

The Money Flow

OpenAI has made crazy infrastructure commitments totaling approximately $1.15 trillion through 2035, broken down as follows:

Broadcom: $350 billion (custom chip design)

Oracle: $300 billion over 5 years (4.5 gigawatts of capacity)

Microsoft Azure: $250 billion (cloud services/credits)

NVIDIA: $100 billion (planned investment partnership)

AMD: $90 billion (GPU purchases, gaining up to 10% stake in AMD)

Amazon AWS: $38 billion over 7 years (cloud infrastructure)

CoreWeave: $22.4 billion (data center capacity)

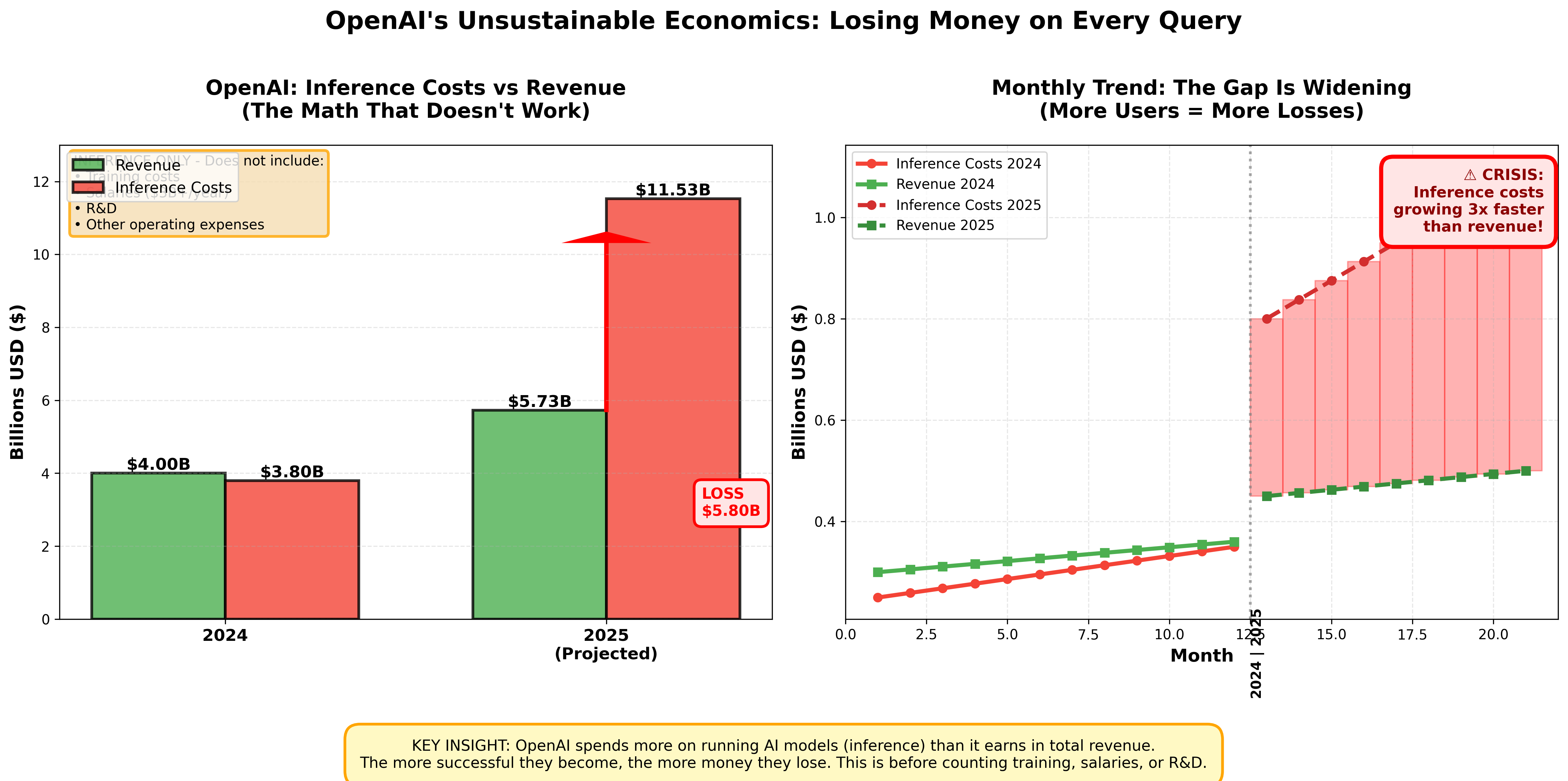

Now, in US you have to live on a big foot. (idk if that make sense, it’s a german saying). OpenAI’s 2025 revenue is projected at only ~$13 billion annually. While the company remains unprofitable with losses of approximately $5 billion in 2024.

The company expects to spend more on inference (running AI models) than it earns in revenue.

Morgan Stanley Research provided a nice overview for this.

What is in it for everyone?

Microsoft

Microsoft is very complex. They invested into OpenAI, are provider, own a stake and get 20% of the revenue of OpenAI and so on.

In other words → Microsoft both invests in OpenAI AND is OpenAI’s largest cloud provider, creating a self-reinforcing loop where Microsoft’s investment helps fund purchases of Microsoft’s own services.

NVIDIA

NVIDIA is somewhat the center water pump for a circular flow. NVIDIA invests in AI companies → Those companies use the money to buy NVIDIA chips → NVIDIA reports strong revenue → Stock price rises → More investment capital available. The investments are going into OpenAI, Anthropic, CoreWave, xAI, Mistral AI, Intel and more.

NewStreet Research estimates that for every $10 billion NVIDIA invests in OpenAI, it expects $35 billion in GPU purchases back. A 3.5x return that raises questions about whether this is an investment or subsidized demand.

Oracle

The big OpenAI Stargate partner comes with an initial equity for the Stargate project and a long-term contract from OpenAI, while building multiple gigawatt-scale data centers in Texas and other locations.

Oracle is borrowing heavily to finance this buildout, expecting OpenAI to generate enough revenue to pay for services. If OpenAI fails, Oracle is left with massive debt and underutilized infrastructure.

SoftBank

Goes big into the Stargate project but also has to borrow against Arm Holdings, liquidating T-Mobile stakes and using its cash reserve.

SoftBank has until year-end 2025 to secure $22.5 billion, and has sold its NVIDIA stake to help fund the venture.

CoreWeave

Despite the contracts and investments with and of OpenAI, Meta, Microsoft, and NVIDIA (and many more), it is just a paradox. CoreWeave spent $1.9 billion in capex in Q3 2025 alone, with projected annual capex of $30 billion in 2026. The company has a capex-to-revenue ratio of 2.3-2.8x, meaning it spends $2.35-$2.77 for every dollar earned. It remains deeply unprofitable despite massive revenue growth.

Amazon, Meta, Google

Also, they are part of investments with OpenAI, they are also driving the diversification in the market.

Amazon invests in Anthropic, and they, in return, commit to using AWS services.

Meta works with CoreWeave, invests heavily in Scale AI, and develops its own model (Llama) as open source.

Google has its own strong ecosystem, data center capacities, its own chips like the TPU, its own AI experts like DeepMind, and so on. Yes, there are also deals here and there with other providers etc, but we could say Google is the most independent from that whole Ring Around the Rosie.

The Bubble Mechanics and Risks

1. Circular financing creates artificial demand

The pattern is remarkably simple and troubling:

NVIDIA invests $100B in OpenAI

OpenAI uses that money to buy NVIDIA chips

NVIDIA reports record revenue from “customer demand”

Stock price rises

NVIDIA has more capital to invest

Repeat

During the dot-com bubble, companies like Global Crossing engaged in “revenue roundtripping” paying other companies for services, who then paid them back in equal amounts for equipment. When the bubble burst, Global Crossing went bankrupt.

2. Massive debt accumulation

Unlike the tech giants (Microsoft, Meta, Google, Amazon) who can fund AI from cash flow, the AI startups are heavily leveraged:

OpenAI: Unprofitable, burning $5 billion/year

CoreWeave: $30 billion capex planned for 2026 vs. ~$5 billion revenue

Oracle: Issuing massive debt to build infrastructure for OpenAI

SoftBank: Borrowing against assets to fund Stargate

(by the way, ALL AI companies are unprofitable, doesn’t matter which one we are talking about)

If AI revenue growth doesn’t materialize, these companies face debt defaults that could cascade through the entire ecosystem. It’s like rock climbers who are chained to each other to prevent them from falling. The problem is, the more that fall, the more it drags others with it.

3. Revenue concentration

The entire ecosystem depends on a tiny number of players. A CoreWeave made 77% of its 2024 revenue from just two customers. OpenAI is burning through investment faster than it grows revenue. And the cloud providers are competing to servce the same AI companies.

If any major player fails or slows spending, the ripple effects would be, well, “interesting”.

4. Valuation disconnect

Ok, so we know that this whole market is not profitable. That’s how US market works. Bigger, louder, better. Fake it until you make it. Everything on Green.

Bain & Company estimates the AI industry needs $2 trillion in annual revenue by 2030 just to justify current infrastructure spending. No problem? This is more than the combined 2024 revenue of Amazon, Apple, Alphabet, Microsoft, Meta, and NVIDIA.

5. The Inference cost problem

Recent leaks show OpenAI may be spending more on inference (running models) than it earns.

This suggests the more customers OpenAI gains, the more money it loses. A fundamentally unsustainable model.

6. Limited outside revenue

Despite billions in investment and trillions in commitments, actual revenue from paying customers remains modest.

OpenAI ChatGPT Plus: 11 million subscribers at ~$20/month = ~$2.6 billion/year

Enterprise customers: Growing but insufficient to cover costs

Most AI products still searching for viable business models beyond subscriptions

MIT Media Lab research found that despite $30-40 billion in enterprise GenAI investment, 95% of organizations are getting zero return.

What do the “Experts” say (warn)?

Michael Burry a “Big Short” investor, is betting against NVIDIA saying it is “Almost all customers are funded by their dealers”. And questions OpenAI’s accounting → “Can anyone name their auditor?”.

Dario Amodei, Anthropics CEO, even as his company participates in circular deals, warns about “players who are YOLOing”. Not sure if this should be a reference to Sam Altman who lives in a world of “Trust me bro”.

Investman analysts like Jay Goldberg, Stacy Rasgon or Ben Inker calls NVIDIA-OpenAI deals “bubble-like behavior”, “The action will clearly fuel ‘circular’ concerns” and “We’re certainly seeing lots of evidence of bubble-like behavior in the AI space”.

The problem is that due to the high stakes and investments a single issue can trigger a collapse. OpenAI can run bankrupt, and I believe that is very likely as the OpenAI CFO in a recent interview danced very long around an asnwer to finally tell us that they are fully open for governmental investments. If circular financing is exposed as artificial demand, NVIDIA’s stock could crash, eliminating the capital fueling the ecosystem. Frankly speaking, imo that is the most obvious thing on the table…

Anyhow, there are multiple scenarious analyst have in sight. From energy constraints, to technical disappointments, regulatory interventions (Europe), or competing technology will promise more (e.g. that LLMs are not the solution for AGI, as promised).

Counterarguments

Ok, we also have to take a look in the other direction. The most discussable point is that AI is delivering actual value, unlike many dot-com companies with no product. To some extent, yes, it does. I personally use it daily, but I can’t tell you, if that makes me really more efficient or not. And then we look at the research of MIT which clearly shows, the investments from companies doesn’t turn around…

OpenAI keeps growing and projects a $20 billion run rate by year-end 2025, potentially $100 billion by 2027…

Microsoft, Meta, Google, Amazon can absorb losses and continue investing. For them it’s a spiel. If OpenAI doesn’t make it, then someone else. And as we see with for example Google, they literally would profit from a failure of OpenAI. This would completely blast away Microsoft from the AI radar. Besides I think unlike worthless stock certificates, data centers and chips retain value. The infrastructure has a residual value, and cloud demand (besides AI) is growing.

Maybe, also the bubble has to do its bubble thing. Because, the internet boom eventually paid off after the bubble; AI could follow the same pattern.

Finaly, the Federal Reserve Chairman Jerome Powell argues AI differs from dot-com because corporations are generating large revenues and driving economic growth. Yet, again I think this is highly discussable. With over 80% AI projects failing, and those who succeed seeing no return on their investment, it might be just a lot of hot air. Reality is what we make from it.

Conclusion - A dangerous Game

The AI boom represents the largest technology investment cycle in history, dwarfing even the dot-com era. But the circular nature of these investments, where the same dollars flow in loops between a handful of players, creates a questionable instability.

The ecosystem works perfectly as long as:

Everyone keeps investing

No one demands profitability

The promise of AGI justifies infinite spending

Stock prices keep rising

But if any link in the chain breaks like OpenAI can’t pay Oracle or CoreWeave’s debt becomes unsustainable or NVIDIA’s revenue is revealed as artificially inflated, the entire structure could collapse with devastating speed.

The question isn’t whether AI will transform the world. It almost certainly will.

The question is whether the current financial architecture supporting that transformation is sustainable or whether we’re building a trillion-dollar house of cards that will leave investors, companies and the broader economy picking up the pieces.

As Anthropic’s Dario Amodei warned: Even if the technology fulfills all its promises, players who get the timing even slightly wrong face catastrophic consequences. With over $1.4 trillion in commitments based on companies that aren’t profitable and revenue models that remain unproven, the margin for error is razor-thin.

The AI revolution may be real. The AI bubble is looking increasingly real as well.